Overhead costs overview

Overhead expenses are indirect costs ( Example electricity) that impact all manufacturing costs, except for direct labor and direct material that change depending on production volume.

Overheads are costs or expenses (such as G&A costs, deprecation, energy, administration, insurance, rent, and utility charges) that:

- Relate to an operation or the company as a unit.

- Do not become an integral part of a good or service (unlike raw material or direct labor).

- Cannot be applied or traced to any specific unit of output.

Overheads are those costs required to run a business, but which cannot be directly attributed to any specific business activity, product, or service. Overhead costs do not directly lead to the generation of profits.

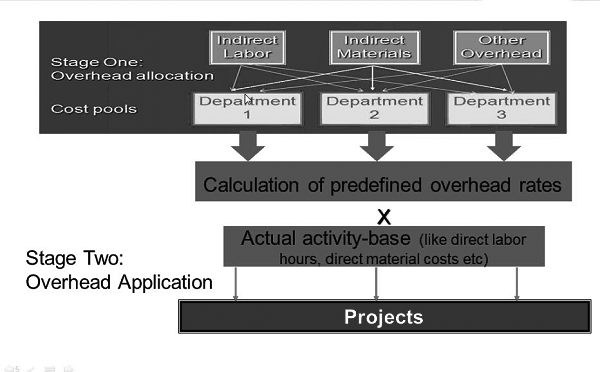

Infor LN allows you to define three types of overhead costs:

Indirect materials

These are costs that indirectly add up to the total cost of an item, such as light, heat, supervision, and maintenance.Indirect labor

Indirect costs such as an hour of labor, administration and general meetings.Miscellaneous expenses

Taxes, insurance, depreciation, repairs, and so on.

Overhead allocation

Overhead allocation is a process of identifying, aggregating and assigning indirect costs to activities, for which organizations want to separately measure costs. The outcome of the overhead allocation process are the overhead rates. Predetermined overhead rates are assumed to be calculated in Excel by dividing the budgeted or estimated overhead with the budgeted activity and are used to apply overhead.

Overhead application bases

For batchwise application of overheads, you must set up bases over which predetermined overhead rates can be calculated.

Calculate overheads

You can calculate overheads on actuals and hard commitments. Set the parameters for overhead calculations in the Project Parameters (tppdm0100s000) session. Note: Hard commitments can only be calculated when the Actuals check box is selected.

Apply overheads

Overheads are applied to price indirect costs of products or projects, so as to cover all costs and thereby generate profits. The result of the overhead application process is that overhead transactions are generated and applied to the related projects and that the journals to be posted to Financials are generated.