Overview of interim revenue recognition in Project Control (PCS)

Products manufactured used projects in Project Control often have long lead times. During the projects, actual costs are recorded. Revenues and cost of goods sold can be determined at the end of the project when the products are finished and delivered.

However, international accounting rules such as IFRS (International Financial Reporting Standards) require greater transparency in business financials. Public companies must be able to recognize costs and revenues not only at the end of the project but also at different times during the project.

With revenue recognition in PCS you can determine the interim revenue and interim COGS for an unfinished project, even before shipping any end item.

These terms are used in interim revenue recognition

Revenue

The gross inflow of economic benefits such as cash, receivables, and other assets during an accounting period. Revenue results from the usual operating activities of an enterprise, for example, sales of goods, sales of services, interest, royalties and dividends.Actual costs

The real costs of production, hours accounting, purchase, service, sales, finance, warehousing or a PCS project.COGS

An accounting classification to determine the amount of direct materials, direct labor, and allocated overhead associated with the products sold during a given period of time.Work-in-Process (WIP)

The value of actual costs and results, subtracted from the COGS posted on the project. The WIP value is used for financial reporting on the balance sheet. When a project is closed, the WIP is cleared.

Percentage of completion

To determine the interim COGS and interim revenues at a specific moment, you must first determine which percentage of the work on the project is completed. You can use three methods to calculate the percentage of completion (POC):

Cost to date

The actual costs to a specific date divided by the estimated total costs at completion. For example, the total estimated costs of the project are $1980,-. The actual costs to the point at which you want to recognize revenue are $200,-. The POC is 200/1980 = 10,1%.Hours progress

The actual hours spent until a specific date divided by the estimated total hours at completion. For example, the total estimated hours of the project are 500. The actual hours until the moment that you want to recognize revenue are 100. The POC is 100/500 = 20%.Manually entered

A percentage that expresses an estimate of the completed work. For example, you estimate that at a specific point, 25% of the work on your project is finished.

This calculation is used to calculate interim revenue at a specific point:

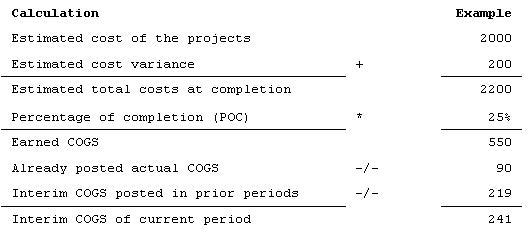

To calculate the interim COGS on a specific point:

Procedure for interim revenue recognition

To calculate interim COGS and revenue, you must go through these of sessions:

- Project Details (tipcs2130m000)

- Calculate Interim COS and Revenues by Project (tipcs3290m000)

- COGS by Cost Component (tipcs3191m000)

- Interim COGS and Revenues by Project (tipcs3190m000)

- Confirm and Post Interim COS and Revenues by Project (tipcs3291m000)

- COGS and Revenues by Project and Order (tipcs3192m000) or COGS and Revenues by Project and Order Line (tipcs3194m000)

The details are described in Recognizing Interim Revenue in Project Control